If you own a restaurant or a catering company, you know that the most exciting part of the job is making great food. You love seeing people enjoy the meals you create. In the past, most restaurant owners only had to worry about the people coming into their dining rooms. They made sure the tables were clean, the floors weren’t slippery, and the kitchen was safe. But today, the food business has changed a lot. Now, a huge part of the business happens outside the four walls of your kitchen.

1. Personal Auto Insurance is Not Enough

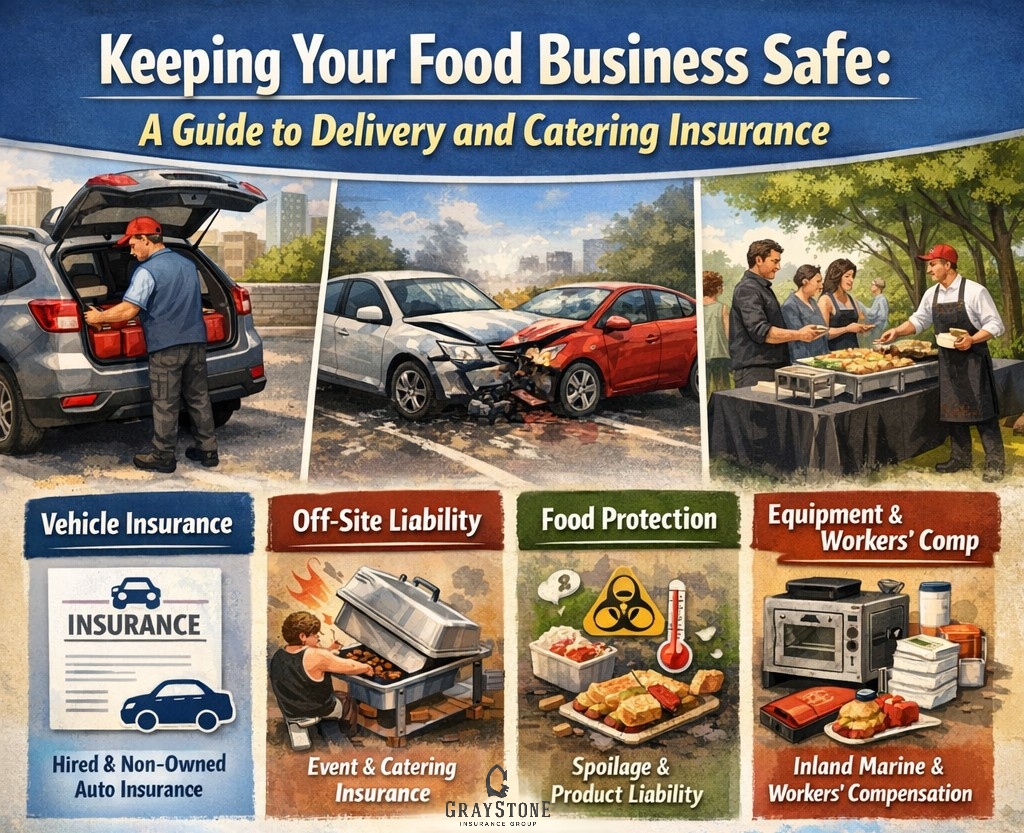

Relying on a driver’s personal car insurance is a major risk. Most personal policies explicitly exclude commercial delivery activities. Business owners must secure Hired and Non-Owned Auto Insurance (HNOA) to protect the company if an employee has an accident while using their own vehicle for work.

2. General Liability is Only the Foundation

While General Liability insurance is essential for basics like slip-and-fall accidents, it isn’t a “catch-all.” You must verify that your policy includes Product Liability to specifically cover foodborne illnesses and food-related injuries.

3. Equipment Needs Protection in Transit

Standard property insurance usually only covers items inside your primary place of business. For caterers, Inland Marine Insurance is necessary to protect expensive kitchen and serving equipment while it is being transported to or used at various event venues.

4. Liquor Liability is a Specific Risk

If your catering service involves serving alcohol, a standard liability policy is insufficient. You need dedicated Liquor Liability coverage to protect against claims related to the actions of intoxicated guests, even if the client provided the alcohol.

5. Plan for “Invisible” Losses

Physical damage isn’t the only threat. Logistics-heavy businesses should consider:

6. Compliance is Non-Negotiable

Workers’ Compensation is legally required in most states for any employee, including part-time delivery drivers. Beyond legal compliance, it is the most effective way to protect your business from the catastrophic costs of workplace injuries.

Many people now use apps on their phones to order dinner, and they expect that food to show up at their front door. Companies want big lunches brought to their offices. Families want birthday parties catered at local parks. While this is great for making money, it also adds new risks. When your food leaves your building, it is “on the road.” This means anything that happens between your kitchen and the customer’s table is your responsibility.

A lot of business owners think their basic insurance covers everything. They think that if they have a policy for their building, they are safe. Sadly, that is not always true. This guide will help you understand the types of insurance you need when you take your food on the road.

The first risk begins the moment the food is loaded into a car. One of the biggest mistakes a restaurant owner can make is letting employees use their own cars for deliveries without the right insurance.

Let’s look at an example. Imagine you have a driver named Sam. Sam is a great worker and uses his own car to deliver bags of food every night. Sam has his own car insurance that he pays for every month. You might think, “If Sam gets into a wreck, his insurance will pay for it.” In almost every case, that is wrong. Most personal car insurance policies have a rule that says they will not pay for any accidents that happen while the person is working for money.

If Sam is driving to the grocery store to buy milk for himself and hits another car, his insurance will pay. But if Sam is driving to a customer’s house with three pizzas in the back seat and hits another car, his insurance company will likely say “no.” They will refuse to pay because he was using his car for a business purpose. When this happens, the person Sam hit will look for someone else to pay the bills. That person is you—the business owner.

To stop this from happening, you need something called Hired and Non-Owned Auto Insurance. This is a special kind of protection. It covers your business if an employee gets into a crash while using their own car for your shop. If your business is big enough to own its own vans or trucks, you need Commercial Auto Insurance. This is just like car insurance for your family, but it is built for businesses that are on the road all day long.

Once the driver arrives, the next set of risks begins. Most people know about “slip and fall” insurance. If a customer walks into your restaurant and slips on a wet floor, your General Liability Insurance pays for their doctor bills. But what happens when that slip happens at someone else’s house or a public park?

Imagine your catering team is setting up a big buffet at a local park. While they are carrying a heavy crate of plates, they accidentally knock over an expensive statue owned by the park. Or, imagine a server spills a tray of hot soup on a guest at a wedding. Because these accidents didn’t happen at your restaurant’s address, your main insurance might not want to pay.

You need to make sure your liability insurance includes “off-premises” coverage. This means your protection follows you like a shadow. Wherever your team goes to serve food, the insurance goes with them. This is very important for caterers who work in homes, offices, and rented halls. You are guests in those places, and if you break something or someone gets hurt, you need to be ready to pay for it.

When food is in your kitchen, you can check the temperature easily. You have refrigerators that stay cold and ovens that stay hot. But once food is in a delivery van, things get harder.

If a delivery driver gets lost and takes an hour to find a house, the food might get to a temperature that makes people sick. If your catering truck breaks down on a highway in the middle of summer, all the meat and dairy in the back could spoil in minutes. This leads to two big problems:

Additionally, if your catering business serves beer, wine, or cocktails, you have even more to think about. In many states, the person who serves the alcohol can be held responsible if something goes wrong. If your staff serves too many drinks to a guest and that guest gets into a car accident on their way home, you might be sued. This is why you need Liquor Liability Insurance. It pays for legal help if you are sued for something related to alcohol.

Caterers use a lot of expensive tools, like portable ovens, high-quality dishes, and silver trays. When you are moving this equipment back and forth in a truck, there is a high chance of it getting damaged. A sudden stop in traffic could send your expensive ovens sliding across the floor of the van, breaking them instantly.

Standard insurance usually covers things that stay inside your building. To cover things on the move, you need Inland Marine Insurance. Don’t let the name fool you—it has nothing to do with boats. It is just a name for insurance that covers property while it is being moved from one place to another.

Finally, you must look after the people who work for you. Delivery drivers and catering crews have very physical jobs. They are lifting heavy boxes, climbing stairs, and driving in bad weather. Workers’ Compensation is a type of insurance that helps your employees if they get hurt on the job. It pays for their doctor visits and gives them some money while they are too hurt to work. While some small businesses try to skip this to save money, it is a big risk. If an employee gets hurt and you don’t have this insurance, they can sue you for everything you own.

In almost all cases, no. Personal auto policies typically exclude coverage for business activities like delivering food for a fee. If an employee gets into an accident while on the clock, their personal insurer will likely deny the claim. To protect your business from these lawsuits, you need Hired and Non-Owned Auto Insurance.

Despite the name, it has nothing to do with the ocean. It is a specific type of coverage for business property that is frequently moved from one location to another. For caterers, this covers your ovens, chafing dishes, and serving equipment while they are in transit or at a client’s venue—items that a standard “property” policy usually only covers while they are inside your main building.

While General Liability covers many “slip and fall” accidents, you should ensure your policy includes Product Liability coverage. This specifically protects you if a customer becomes ill or injured due to the food or drink you served. For caterers and delivery services, this is one of the most critical components of your safety net.

Yes. If your staff is serving the alcohol—even if you didn’t sell the bottles yourself—your business can still be held liable for the actions of an intoxicated guest under many state “Dram Shop” laws. Liquor Liability Insurance is essential for any catering team that handles or serves alcoholic beverages.

Standard insurance policies rarely cover the loss of the food itself due to mechanical failure or power loss. Spoilage Insurance is a specific add-on that reimburses you for the cost of ingredients and prepared food that must be thrown away because of a refrigeration failure or a breakdown during transport.

In most states, yes. Any employee, whether full-time or part-time, is usually required to be covered by Workers’ Compensation. Because delivery and catering involve driving, lifting, and working in high-pressure environments, the risk of injury is higher, making this coverage vital to avoid massive medical debt or legal action.

Running a food delivery or catering business is a great way to grow your brand and reach new customers. It allows you to share your cooking with the whole community. However, as your business moves out into the world, the risks move with it. From car accidents to food safety, there are many things that can go wrong when you aren’t under your own roof.

The good news is that you don’t have to face these risks alone. By getting the right insurance, you are putting a safety net around your hard work. You are making sure that one mistake or one accident won’t ruin everything you have built. Insurance gives you the peace of mind to focus on what you do best: making delicious food.

If you aren’t sure if your business is fully protected, now is the time to find out. Don’t wait until after an accident happens to check your paperwork. At GrayStone Insurance Group, we know the food industry inside and out. We can look at your current plan and help you find any hidden risks. We will work with you to create a plan that fits your budget and protects your future. Give us a call today or visit our office to start your free review. Let us handle the insurance so you can get back to the kitchen!