The article emphasizes that managing risk effectively is the most important defense against costly lawsuits and high insurance premiums.

A successful bar or music club is full of fun—bright lights, loud music, and a dance floor packed with people. That energy is great for business! But under all that fun, there is a big risk of things going wrong.

Because you serve alcohol, deal with big crowds, and stay open late, your business faces a lot of legal and financial trouble that regular stores do not. If something big happens—like a guest getting too drunk, a fight breaking out, or someone falling and getting hurt—it could cause an expensive lawsuit that could close your business.

Your regular insurance policy (Commercial General Liability or CGL) only covers small, everyday problems. At GrayStone Insurance Group, we know that great safety rules are what help you keep claims low. When claims are low, your insurance costs less, especially for your General Liability and Liquor Liability policies.

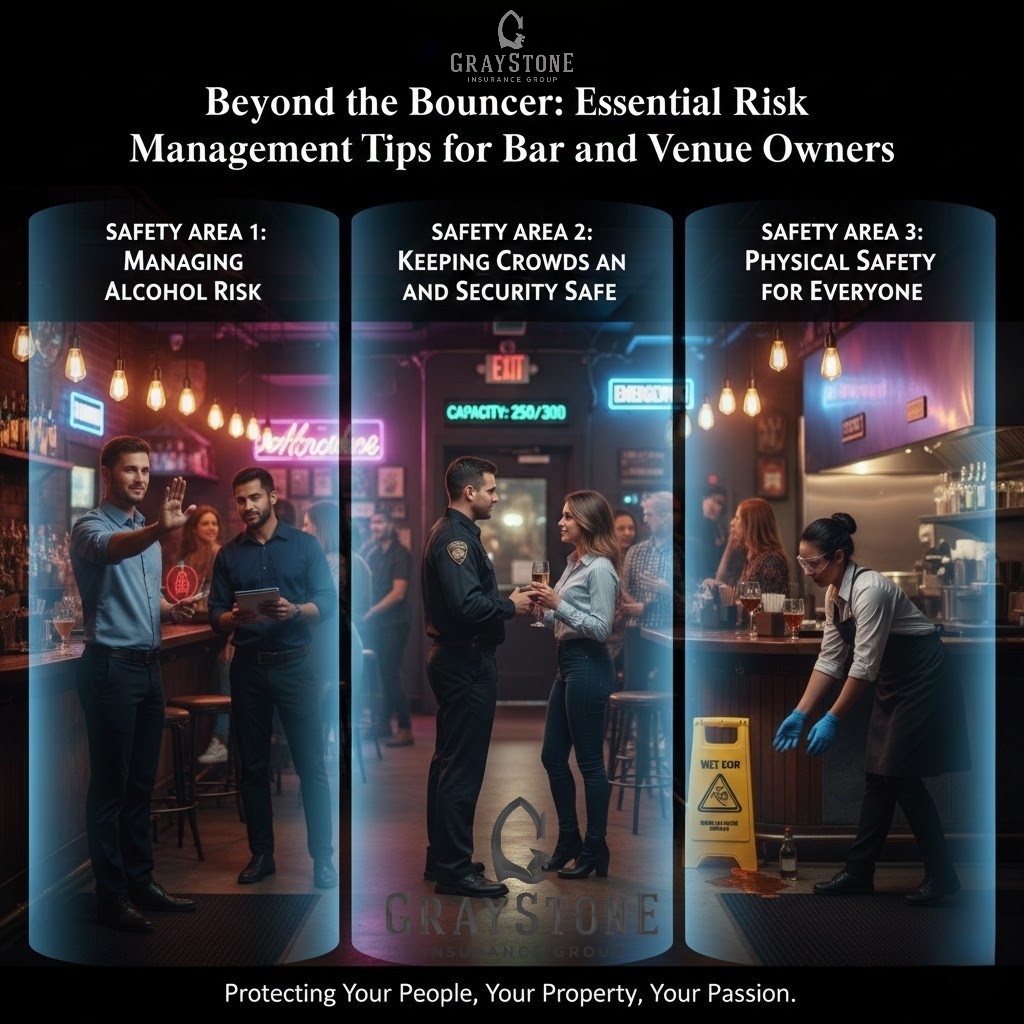

The best way for you to protect your business against expensive lawsuits is to have clear, written-down safety steps that you always follow in three main areas: Serving Drinks, Security, and Keeping the Building Safe.

Serving alcohol is the single biggest risk for your business. Laws like Dram Shop Liability say that if you sell drinks to someone who is clearly drunk, and that person later causes an accident, you can be sued for all the damage they caused. You must follow all the rules for serving drinks if you want your business to survive.

Your first line of defense against lawsuits is training your people. It’s not enough to hire people who have worked at bars before; every person on your team must be certified in an official program (like TIPS or TAM) on how to serve alcohol safely.

Your staff must be given the power to stop serving drinks, even if the business loses a sale. Safety comes first.

If you ever get sued because of Dram Shop laws, your paperwork is your only proof that you did the right thing. If you don’t write it down, the court will think you didn’t do it.

Fights, injuries from too many people in one place, and security using too much force are the main reasons for very expensive Commercial General Liability claims.

You must be in full control of who comes into your building and how many people are inside.

Your security team should be trained to calm people down instead of getting into physical fights. The main goal is to stop problems before they get violent.

Asking a person to leave is a high-risk action. Lawsuits for fighting or using too much force are common if you don’t follow rules.

Controlling the physical space is key to stopping common, but expensive, Commercial General Liability claims (like slips and falls) and protecting your staff from getting hurt (Workers’ Compensation claims).

Floors in bars are always dangerous because of spills. This causes many CGL claims.

Not following basic fire and emergency rules is a major cause of lawsuits.

The physical work of running a bar means you need safety rules to keep Workers’ Compensation claims low.

These questions and answers summarize the most critical risk and insurance points for bar and club owners, based on the provided safety guide.

I. Alcohol and Legal Liability

Q: What is Dram Shop Liability and why is it the biggest risk?

A: Dram Shop Liability is a law in many states that allows your business to be sued if you serve alcohol to a customer who is visibly drunk, and that customer later causes an accident (like a car crash or an injury). It’s the biggest risk because the lawsuits can hold your business financially responsible for all the damages caused by the intoxicated person.

Q: Does my entire staff need alcohol service training?

A: Yes. The article recommends that everyone who handles alcohol or checks IDs—including bartenders, servers, managers, and security—must be certified in a recognized program (like TIPS or TAM). This training is your first line of legal defense.

Q: What is the most important part of refusing service to a drunk customer?

A: The most critical step is documenting the refusal immediately in an Accident Report and taking reasonable steps to ensure the person gets home safely (like calling them a taxi or ride-share). If you don’t write it down, the court will assume you didn’t do it.

II. Insurance Coverage and Protection

Q: What is the difference between Commercial General Liability (CGL) and Liquor Liability insurance?

A: Commercial General Liability (CGL) covers non-alcohol-related accidents, such as a slip-and-fall injury or property damage. Liquor Liability is a specific policy that covers claims directly resulting from the sale and service of alcohol, particularly related to Dram Shop laws. Both are essential for bars and clubs.

Q: How do strong safety rules lower my insurance costs?

A: Insurance companies offer lower premiums (prices) to businesses with lower risk. When you can prove you have a strong, consistent commitment to safety—through certified training records, detailed incident reports, and cleaning logs—you show the insurer you are actively reducing the chance of costly claims.

III. Security and Physical Safety

Q: What should security focus on during a high-tension situation?

A: Security teams should focus on de-escalation—using calm words and body language to stop problems before they become violent fights. Physical force should only be used as a last resort, and must be the “smallest amount of force needed” for ejection, as excessive force leads to high legal costs and potential lawsuits.

Q: What is the biggest physical safety risk in a bar or club?

A: Slips and falls are the most common and costly source of CGL claims due to constant spills, melting ice, and wet floors. This risk must be addressed by having a mandatory, written schedule for checking and cleaning floors in busy areas every 15 to 20 minutes.

Q: Can I exceed my building’s fire code capacity if it’s a popular night?

A: No, never. Managers must know the legal fire code limit and strictly adhere to it. Exceeding capacity is a major safety violation, a huge risk for mass injury, and can cause your insurance provider to refuse to pay any claim if an incident occurs.

A successful club needs more than great service; it needs a strong, consistent commitment to documented safety.

The accident reports, training papers, and cleaning lists are not just simple tasks—they are the only proof your insurance company can use to defend you in court. When you can show that you followed a reasonable set of safety standards, you greatly improve your legal position.

Your Insurance Advantage: When you prove to your insurance company that you are serious about safety (by showing proof of certified training and detailed response logs), you lower the risk of your venue. This leads directly to lower prices and better plans for your most important insurance: the Commercial General Liability and Liquor Liability policies.

Don’t let the cost of prevention stop you. Contact GrayStone Insurance Group today for a comprehensive risk check. We will help you put together the strong safety procedures and paperwork needed to protect your investment and secure the best coverage for your venue.